How African Commodities Are Shaping Global Supply Chains: The Untold Economic Revolution

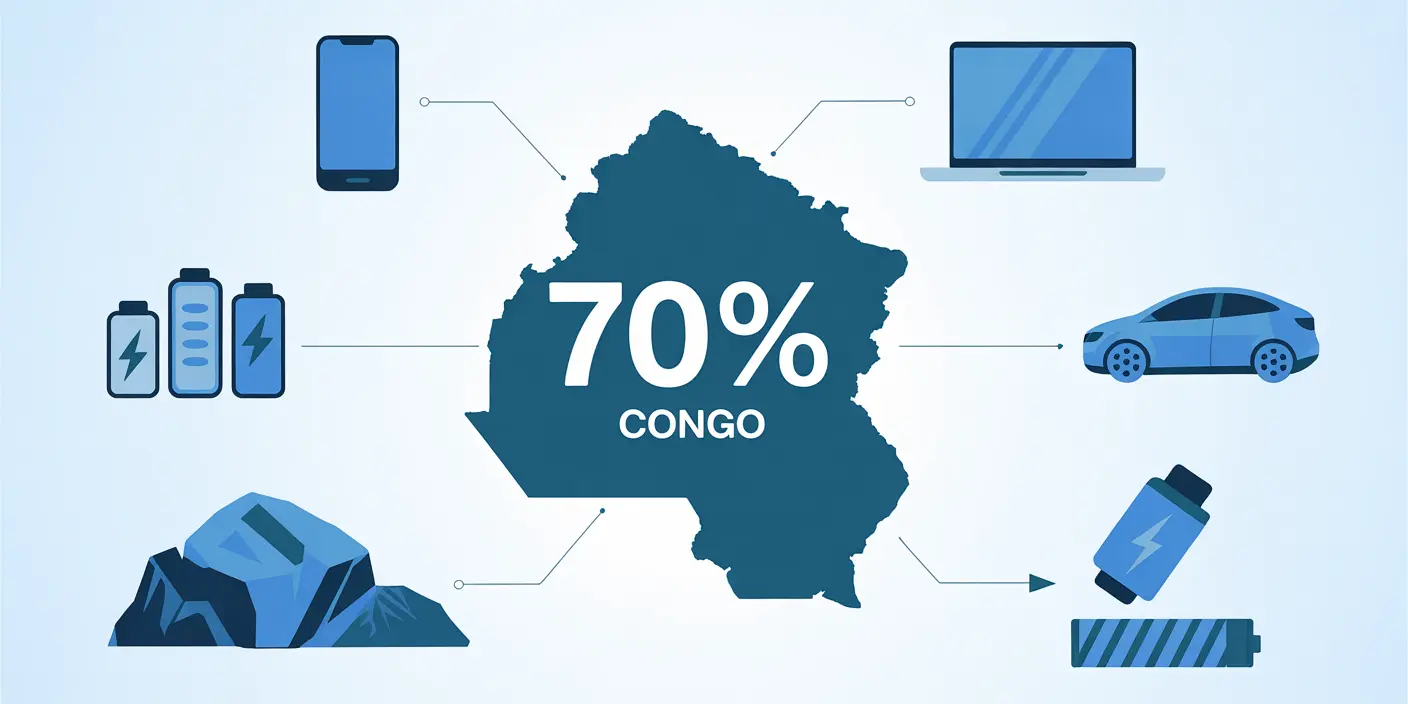

Here’s something that’ll blow your mind: the smartphone in your pocket, the electric car your neighbor just bought, and even that chocolate bar you had for lunch? They all have something in common—they probably couldn’t exist without Africa. I remember sitting in a supply chain conference about three years ago when a speaker dropped this bombshell: nearly 70% of the world’s cobalt comes from one country in Africa. One country! I almost spit out my coffee.

The thing is, most people have no idea just how dependent our modern global economy has become on African commodities. We’re not just talking about diamonds and gold anymore—though those are still pretty important. We’re talking about the minerals that power your laptop, the cocoa that makes your morning bearable, and the lithium that’s gonna fuel the electric vehicle revolution. Africa isn’t just participating in global supply chains; it’s literally holding the keys to some of the most critical resources on the planet.

I’ve spent the better part of a decade studying international trade patterns, and honestly, the shift I’ve witnessed has been nothing short of revolutionary. When I started out, Africa was often dismissed as a peripheral player in global commerce. Now? Major corporations are scrambling to secure long-term supply agreements with African nations, governments are redrawing their strategic resource maps, and the entire conversation around supply chain resilience has Africa front and center. The crazy part is that most consumers have no clue this is happening behind the scenes.

So why should you care? Whether you’re a business owner trying to understand future supply risks, an investor looking for the next big opportunity, or just someone curious about how the world really works, understanding Africa’s role in global supply chains isn’t optional anymore—it’s essential. Let’s dive into this transformation that’s reshaping everything from your tech gadgets to international politics.

The Rising Dominance of African Minerals in Tech Supply Chains

Okay, so let me tell you about the moment I realized just how screwed the tech industry would be without African minerals. I was consulting for a mid-sized electronics manufacturer, and they were panicking—absolutely panicking—because their cobalt supplier in the Democratic Republic of Congo had just experienced a temporary shutdown. Production lines stopped. Deadlines got missed. Money was lost. All because of one mineral from one region.

The Democratic Republic of Congo controls roughly 70% of the world’s cobalt supply, and cobalt is absolutely essential for lithium-ion batteries. Every single smartphone, laptop, and electric vehicle relies on this stuff. I’ve watched companies try to diversify their cobalt sources for years, and guess what? There just aren’t that many alternatives. Australia produces some, and there are deposits in Canada, but the DRC remains king. It’s like they’ve got a monopoly on the future of technology, whether they meant to or not.

But cobalt’s just the beginning. Zimbabwe’s sitting on some of the largest lithium deposits in the world—we’re talking about the stuff that’s gonna power the electric vehicle revolution. I made a huge mistake early in my career by underestimating how quickly EV adoption would happen, and now I’m watching African lithium become more valuable than I ever imagined. The Bikita deposit alone could change Zimbabwe’s entire economic trajectory.

Then there’s the rare earth elements situation, which honestly keeps supply chain managers up at night. These aren’t as concentrated in Africa as cobalt, but countries like South Africa, Malawi, and Tanzania have significant deposits. Rare earths are used in everything from wind turbines to guided missiles, and the fact that China currently dominates processing? That’s made African deposits incredibly strategic. I’ve seen governments quietly scrambling to secure partnerships before their competitors do.

Here’s where it gets messy though—and this is something I’ve struggled with personally. The mining operations extracting these minerals often have serious environmental and ethical issues. Child labor in cobalt mines is well-documented. Environmental degradation is rampant. Water contamination affects local communities. I’ve visited some of these regions, and the disconnect between the gleaming tech products we use and the conditions under which their components are extracted is… it’s honestly heartbreaking. Tech companies are under increasing pressure to ensure ethical sourcing, but the supply chains are so complex that even they sometimes don’t know exactly where their minerals come from.

The dependency is only growing stronger. As we transition to renewable energy and electric transportation, demand for these African minerals is projected to increase by 500% or more over the next two decades. The power dynamics this creates are fascinating and terrifying at the same time. African nations suddenly have leverage they’ve never had before, and tech companies are realizing that their entire business models depend on stable access to resources from regions they don’t control.

Agricultural Commodities: Africa’s Traditional Stronghold

I’ll never forget my first trip to Côte d’Ivoire’s cocoa farming regions. The smell of fermenting cocoa beans, the endless plantations stretching to the horizon, and the realization that this relatively small country produces nearly 40% of the world’s cocoa—it completely changed how I look at my chocolate consumption. West Africa, particularly Côte d’Ivoire and Ghana combined, controls about 60% of global cocoa production. Your Snickers bar, your hot chocolate, that fancy artisan chocolate shop downtown? All probably started in West Africa.

The interesting thing about agricultural commodities is that Africa’s been dominant here for way longer than in minerals. But the supply chains have become way more sophisticated and, honestly, more vulnerable. I learned this the hard way when I was advising a European chocolate manufacturer and climate change hit their supply chain hard. Irregular rainfall patterns, rising temperatures, and new pest diseases decimated yields in some regions. We had to completely rethink sourcing strategies, and it wasn’t pretty.

Coffee is another massive export, particularly from Ethiopia and Kenya. Ethiopian coffee has this almost mythical reputation among coffee snobs—it’s where coffee originated, after all. I’m personally addicted to Kenyan AA beans, which probably says more about me than I’d like to admit. But here’s what most people don’t realize: these coffee supply chains support millions of smallholder farmers whose entire livelihoods depend on global commodity prices they have zero control over. When prices crash, which happens regularly, entire communities suffer.

Cotton production across the Sahel region—countries like Mali, Burkina Faso, and Benin—is another crucial supply chain that doesn’t get enough attention. These countries compete with massive subsidized cotton producers in places like the United States, which creates this totally unfair market dynamic that I’ve seen devastate African farmers. The cotton ends up in clothing manufactured in Asia and sold globally, making it this perfect example of how interconnected and complicated modern supply chains have become.

Cashew nuts present a particularly frustrating case study that I reference constantly. Africa produces the majority of raw cashew nuts globally, but most of them get shipped to Vietnam and India for processing. Why? Because those countries invested in processing infrastructure decades ago while African nations focused on raw export. The result is that Africa captures only a tiny fraction of the value chain. It’s left money on the table for generations, and only recently have countries like Côte d’Ivoire and Tanzania started building domestic processing capacity. Better late than never, I guess, but man, what an opportunity cost.

Climate change is the elephant in the room for all agricultural commodities. I’ve watched projections that suggest traditional growing regions might become unsuitable within a few decades. Some crops might need to shift to different latitudes or altitudes entirely. The supply chain disruptions this could cause are staggering to think about. We’re talking about potentially displacing millions of farmers and completely restructuring commodity flows that have existed for over a century.

Energy Resources Reshaping Global Power Dynamics

Energy commodities are where things get really geopolitical really fast, and I’ve seen some wild shifts here. Nigeria and Angola have been major oil producers for decades—Nigeria’s actually Africa’s largest oil producer and was a cornerstone of global energy markets for years. I remember when Nigerian crude was considered premium quality, commanding top prices. But the industry there has faced so many challenges: pipeline vandalism, corruption, aging infrastructure, and the messy transition away from fossil fuels globally.

Angola’s oil production has actually been declining, which I find fascinating from a supply chain perspective. They peaked around 2008 and have been on a downward trajectory since. Meanwhile, global demand patterns shifted, new producers emerged, and suddenly Angola’s trying to diversify its economy after depending on oil for like 95% of export revenue. Talk about putting all your eggs in one basket—I use this as a cautionary tale constantly.

Natural gas is where the real excitement is now though. Mozambique and Tanzania have enormous offshore gas reserves that were discovered relatively recently. We’re talking about reserves that could transform these countries from some of the poorest in the world into energy exporters rivaling Middle Eastern nations. I’ve watched multinational energy companies pour billions into development projects there. But here’s the kicker—militant insurgency in northern Mozambique has delayed projects repeatedly, which perfectly illustrates how political instability can derail even the most promising supply chain opportunities.

The renewable energy potential across Africa is absolutely mind-blowing and criminally underutilized. The solar potential in the Sahara alone could theoretically power the entire planet—not that we’d actually do that, but the numbers are just ridiculous. Wind resources along coastlines, massive hydroelectric potential in the Congo Basin, geothermal energy in the East African Rift Valley. I’ve seen estimates suggesting Africa could become a net energy exporter through renewables within a few decades if the investment happens.

But here’s the paradox that frustrates me: Africa has enormous energy resources yet hundreds of millions of Africans lack reliable electricity access. It’s this weird situation where energy is being extracted and exported while local populations remain energy-poor. I consulted on an energy project once where we were literally building infrastructure to export gas while nearby communities still used kerosene lamps. The disconnect was jarring.

The transition from fossil fuels to green energy is creating this whole new dynamic too. Suddenly the minerals needed for solar panels, wind turbines, and batteries are more valuable than the oil and gas themselves. Countries that invested everything in fossil fuel extraction are scrambling to position themselves in the new energy economy. Some will succeed. Others will be left behind with stranded assets and economies built on obsolete industries. It’s creative destruction on a continental scale, and honestly, it’s sometimes hard to watch.

Critical Minerals for the Green Energy Transition

This section is where I get really excited because the green energy transition has completely flipped the script on which resources matter most. I’ve been following this space closely, and the numbers are just staggering. The International Energy Agency projects that demand for critical minerals could increase by 400-600% by 2040 just from clean energy technologies. And guess where a huge percentage of those minerals are? You got it—Africa.

Cobalt and copper are the superstars here. We already talked about Congolese cobalt, but the DRC also has significant copper deposits, as does Zambia. Copper is essential for electrical wiring in everything from EVs to wind farms to solar installations. I watched copper prices absolutely skyrocket during the pandemic supply chain crisis, and that’s probably just a preview of future volatility. The Zambian Copperbelt has been mined for over a century, but it’s getting renewed attention and investment now because demand projections are through the roof.

South Africa’s platinum group metals (PGMs) are another critical piece. Platinum, palladium, and rhodium are used in catalytic converters, hydrogen fuel cells, and various industrial processes. South Africa produces about 70-80% of the world’s platinum and has the largest PGM reserves globally. I’ve watched the mining sector there struggle with labor disputes, energy shortages, and aging infrastructure, but the strategic importance of these metals means investment keeps flowing. It’s too important to global supply chains to fail.

Mozambique’s graphite deposits are massive and increasingly important. Graphite is used in battery anodes for electric vehicles, and synthetic graphite production is energy-intensive and expensive. Natural graphite from Mozambique offers a more cost-effective alternative. I’ve seen projections suggesting Mozambique could become one of the world’s largest graphite producers within this decade. The Balama project alone could supply a significant portion of global demand.

Manganese is less glamorous but absolutely essential for steel production and increasingly for battery technology. South Africa and Gabon have enormous manganese deposits. Steel manufacturing obviously needs manganese, but the new lithium-ion battery chemistries are increasingly using manganese to reduce cobalt content—partly because of cobalt’s ethical issues and partly because it’s so expensive. This shift could make manganese even more strategically important than it already is.

Here’s what keeps me up at night though: the entire green revolution that’s supposed to save us from climate change is completely dependent on these African resources. But extracting them often causes significant environmental damage—mining, processing, water use, habitat destruction. It’s this painful irony where the solution to one environmental crisis potentially creates or exacerbates others. I don’t have easy answers here, and anyone who claims to is probably oversimplifying.

The concentration of these resources also creates geopolitical vulnerabilities. What happens if major producing regions become unstable? What if countries decide to restrict exports to build domestic processing industries? What if labor disputes shut down critical mines? I’ve modeled various scenarios, and almost all of them involve significant supply chain disruptions and price spikes that ripple through the entire global economy. The transition to green energy is necessary, but the supply chain dependencies it creates are genuinely concerning.

Supply Chain Challenges and Infrastructure Gaps

Alright, let’s talk about the unglamorous but absolutely critical infrastructure problems that plague African commodity supply chains. I’ve personally experienced these frustrations more times than I can count. Africa has the resources the world desperately needs, but getting them from the mine or farm to global markets? That’s where everything often falls apart.

Port congestion is a massive, constant headache. I once had a shipment of agricultural products sit in Dar es Salaam port for three weeks beyond schedule because of congestion and bureaucratic delays. Three weeks! In international commodity trading, timing is everything, and that kind of delay cost my client serious money. Major African ports like Lagos, Mombasa, and Durban regularly experience congestion that would be considered catastrophic in places like Singapore or Rotterdam. Limited berths, outdated equipment, inefficient processes—it all adds up to massive bottlenecks.

The road and rail infrastructure situation is even more challenging. I’ve traveled on roads that were barely roads—more like suggestions of where a road might someday exist. Landlocked countries face particularly brutal challenges. Getting copper from Zambian mines to port can be an absolute nightmare. Rail networks that were built during colonial times haven’t been adequately maintained or expanded. Some critical routes have single-track rail lines that create constant bottlenecks. I’ve seen commodity shipments delayed by weeks simply because of infrastructure limitations.

Political instability adds another layer of complexity that’s really hard to plan around. I learned this lesson painfully when a coup in one African country completely disrupted supply chains I’d spent months carefully organizing. Suddenly border crossings closed, officials changed, regulations shifted, and existing agreements became questionable. Companies want reliable, predictable supply chains, and political instability is the antithesis of that. It creates risk premiums that make African commodities more expensive and less attractive despite their strategic importance.

Corruption and transparency issues permeate many African commodity supply chains. I’ve witnessed situations where unofficial “fees” had to be paid to move shipments through customs, where licensing processes were deliberately slowed until payments were made, where contracts suddenly needed “renegotiation” with new government officials. It’s frustrating, it’s expensive, and it creates enormous uncertainty. International companies often struggle with this because they’re bound by anti-corruption laws in their home countries but face different realities on the ground.

The digital infrastructure gap is something people often overlook but it’s increasingly critical. Modern supply chains rely on real-time tracking, data analytics, digital documentation, and instant communication. Many African regions still lack reliable internet connectivity, have inconsistent electricity, and haven’t digitized customs and regulatory processes. I’ve tried to implement supply chain tracking systems that just couldn’t function properly because the digital infrastructure wasn’t there. You can’t optimize what you can’t track, and you can’t track what isn’t connected.

Despite all these challenges—or maybe because of them—there’s enormous investment flowing into African infrastructure right now. China’s Belt and Road Initiative has funded massive port, rail, and road projects. Other countries and development institutions are investing billions. Things are genuinely improving in many regions, but infrastructure development takes time and the commodity demand is growing right now. There’s this race between infrastructure improvement and demand growth, and I’m honestly not sure which is winning.

China’s Strategic Investment in African Commodity Supply Chains

I need to be real with you—China’s footprint across African commodity supply chains is absolutely massive, and it’s reshaping global economic relationships in ways that’ll matter for decades. I’ve watched this unfold firsthand through multiple projects, and the scale and strategic thinking behind it is impressive, concerning, or both depending on your perspective.

The Belt and Road Initiative in Africa is way more than just some feel-good infrastructure program. It’s strategic resource security wrapped in development financing. I’ve seen Chinese companies build entire rail lines from landlocked mines to coastal ports, construct massive port facilities, and develop entire economic zones—all with the implied or explicit understanding that commodity exports will flow to China. The Addis Ababa-Djibouti railway? Chinese built and financed. The expansion of numerous African ports? Chinese money and construction. These aren’t random acts of generosity; they’re calculated investments in securing long-term resource access.

Mining rights and long-term supply agreements are where things get really interesting. Chinese companies have secured massive stakes in African mining operations across the continent. In the DRC alone, Chinese companies control or have significant interests in 15 of the 19 cobalt-producing mines. That’s not an accident—that’s strategy. They identified cobalt as critical for future technology decades ago and systematically acquired access. I’ve watched Western companies and governments suddenly realize they’re way behind in this game, and now they’re scrambling to catch up.

The infrastructure-for-resources model is China’s signature approach. They’ll finance and build the infrastructure a country needs—roads, railways, ports, power plants—often with loans that use future commodity exports as collateral. It’s clever, but it’s also created what some call “debt trap” situations where countries end up owing enormous sums to Chinese lenders with limited flexibility if things go wrong. I’ve seen countries struggle with this balance between much-needed infrastructure development and maintaining economic sovereignty.

Western concerns about commodity security are totally valid and growing louder. If China controls or has preferential access to the majority of critical minerals the world needs for technology and green energy, that creates enormous strategic vulnerability for other countries. I’ve been in meetings where this is discussed with genuine alarm—what happens if geopolitical tensions escalate and China restricts access to resources it controls? The entire green energy transition in Western countries could be compromised. It’s the kind of dependency that makes security analysts really nervous.

But alternative partnerships are emerging, though they’re playing catch-up. The U.S. has been increasing its engagement with African nations around critical minerals through initiatives like Prosper Africa. The European Union has been pushing its Global Gateway program as an alternative to Belt and Road. India is expanding its African footprint. Australia is sharing mining expertise and technology. These efforts are real, but China got a decade-plus head start and built relationships while others were relatively disengaged.

Here’s my take after watching this unfold for years: China saw the future of global supply chains earlier and positioned itself aggressively. Other countries are now realizing that commodity access is about national security, not just economics. The competition for African resources and relationships is intensifying, which could be good for African nations if they can leverage competing interests for better terms. But it also creates pressure and complexity in already challenging operating environments. This dynamic is going to shape international relations for the foreseeable future.

The Impact of African Continental Free Trade Area (AfCFTA)

Okay, so the African Continental Free Trade Area—or AfCFTA if you want to sound like you know what you’re talking about at cocktail parties—officially launched in January 2021, and honestly, it could be a complete game-changer for African commodity supply chains. I say “could be” because implementation is still early and, let’s be real, plenty of ambitious trade agreements have failed to live up to their potential. But the concept is solid and the potential is enormous.

The basic idea is creating a single market for goods and services across 54 African countries with a combined population of 1.3 billion people and a GDP of about $3.4 trillion. For commodity supply chains, this is potentially revolutionary because it dramatically reduces barriers to intra-African trade. I’ve watched African countries trade more with Europe, China, or the U.S. than with their neighbors for years—sometimes because it was literally easier and cheaper to ship commodities overseas than across borders within Africa. AfCFTA is supposed to change that.

Intra-African trade opportunities are the most exciting part from a supply chain perspective. Why should copper from Zambia get shipped to China for processing when it could potentially be processed in South Africa or Egypt? Why should raw cashews from Tanzania go to Vietnam instead of being processed in Kenya? By reducing tariffs and non-tariff barriers, AfCFTA creates opportunities for regional value chains that keep more economic activity and value on the continent. I’ve consulted with companies exploring exactly these opportunities, and the enthusiasm is real.

Value addition and processing within the continent is where the real economic transformation could happen. For decades, Africa has exported raw commodities—ore, beans, crude oil—and imported finished products made from those very commodities. It’s left billions of dollars of value on the table. AfCFTA creates incentives and frameworks for building processing capacity within Africa. I’ve seen proposals for integrated mining and processing operations, agricultural value chains that include processing and packaging, and manufacturing clusters that serve regional markets. If even a fraction of these materialize, the impact would be substantial.

Reducing dependence on single export markets is crucial for commodity exporters. I’ve watched countries suffer when their primary export market experiences economic problems or when political relationships deteriorate. AfCFTA provides diversification opportunities—multiple markets, multiple buyers, multiple supply chain routes. That resilience is valuable and something commodity producers should have developed years ago. Better late than never.

The job creation and economic diversification potential is what gets development economists excited. Processing and manufacturing create more jobs than raw commodity extraction. They develop technical skills, build institutional capacity, and create opportunities for entrepreneurship. If AfCFTA successfully encourages value addition, it could create millions of jobs and help African economies diversify beyond raw commodity dependence. That’s been the dream for decades, and maybe—just maybe—the conditions are finally aligning for it to happen.

But let me inject some reality here because I’ve been around long enough to be skeptical of overly optimistic projections. Implementation challenges are enormous. Countries need to actually ratify and implement the agreement, which some haven’t fully done. Infrastructure gaps still exist—you can reduce tariffs all you want, but if there’s no reliable way to transport goods between countries, it doesn’t matter. Political will could waver if countries perceive they’re losing out. And established supply chains don’t reorganize overnight; there’s massive inertia in existing trade patterns. AfCFTA is a framework and an opportunity, but realizing its potential requires sustained effort, investment, and cooperation. We’ll see.

Sustainability and Ethical Sourcing Pressures

This is the section that makes me uncomfortable, and that’s probably good because it should make everyone uncomfortable. The sustainability and ethical issues in African commodity supply chains are serious, well-documented, and improving way too slowly. I’ve visited mining operations and farming communities where the gap between the glossy corporate sustainability reports and the actual conditions on the ground is… let’s just say it’s substantial.

Child labor in cobalt and cocoa supply chains is probably the most publicized issue, and rightfully so. Estimates suggest tens of thousands of children work in cobalt mines in the DRC, often in dangerous artisanal mining operations with minimal safety equipment or protections. In West African cocoa, estimates run even higher—potentially over a million children involved in cocoa production, many in hazardous conditions. I’ve seen the defensive responses from chocolate and tech companies when confronted with this reality, and while many are genuinely trying to address it, progress has been painfully slow. The supply chains are complex, visibility is limited, and economic desperation drives families to rely on child labor despite the risks.

Environmental degradation from mining operations is another massive issue I’ve witnessed firsthand. Open-pit mining operations that destroy forests and agricultural land. Water sources contaminated with heavy metals and processing chemicals. Entire ecosystems damaged or destroyed. I visited a region downstream from several mines where the river was literally a different color and nothing would grow in the soil near the banks. Local communities that depended on that water and land for generations had their livelihoods destroyed. The mining company paid some compensation—nowhere near adequate—and moved on. That image haunts me.

Corporate responsibility and traceability initiatives have proliferated in response to pressure from consumers, activists, and regulators. Every major company seems to have a sustainability program, ethical sourcing commitments, and targets for responsible supply chains. Some are genuinely meaningful and making real progress. Others are, frankly, greenwashing—creating the appearance of responsibility without fundamental change. I’ve worked with both types, and you can tell the difference pretty quickly based on whether they’re willing to make hard choices that might increase costs or reduce profits in service of ethical objectives.

Certification programs like Fairtrade, Rainforest Alliance, the Responsible Cobalt Initiative, and others attempt to create standards and verification for ethical practices. These can be effective, but they’re also imperfect. Certification costs money that small-scale producers often can’t afford. Audits can be superficial or focus on paperwork compliance rather than actual conditions. Fraudulent certificates exist. I’ve seen certified operations that still had serious issues and uncertified operations that were actually doing better. Certification is a tool, not a guarantee, and consumers should understand that.

Consumer demand for ethical products is growing, which creates market pressure for improvement, but there’s also a major disconnect. People say they care about ethical sourcing, but many aren’t willing to pay significantly more for ethically sourced products. I’ve seen market research showing this gap between stated values and actual purchasing behavior repeatedly. Companies respond to what consumers actually do, not what they say they care about in surveys. If we want ethical supply chains, consumers need to put their money behind those values even when it means paying more or accepting less convenience.

Here’s the brutal truth I’ve learned: fixing these sustainability and ethical issues requires fundamental changes to how commodity supply chains operate and how value is distributed. It requires paying more to producers so they’re not economically desperate. It requires investing in proper mining infrastructure and regulation rather than allowing artisanal operations to fill the gap. It requires transparency and accountability that some companies resist because it reveals uncomfortable truths. It requires consumers accepting higher prices. These aren’t easy or comfortable changes, and progress will be slow and uneven. But the alternative—continuing to build our prosperity on exploitation and environmental destruction—is morally indefensible. We can do better, and we must.

Technology and Innovation in African Commodity Trading

Technology is starting to transform African commodity supply chains in ways that honestly would have seemed like science fiction a decade ago. I’ve gone from dealing with paper-based documentation and weeks-long communication delays to real-time tracking and instant settlements, and the pace of innovation just keeps accelerating. It’s exciting, though implementation remains uneven across the continent.

Blockchain for supply chain transparency is probably the most hyped technology application, and for once, some of the hype might be justified. I’ve worked on blockchain pilots that track minerals from mine to manufacturer, creating an immutable record of custody and origin. The transparency this creates is potentially revolutionary for addressing ethical sourcing concerns. If you can verify that cobalt came from a certified mine with proper labor practices rather than an artisanal operation using child labor, that’s enormously valuable. Companies like De Beers have been using blockchain to track diamonds, and similar applications are expanding to other commodities. The technology works; the challenge is getting universal adoption across fragmented supply chains.

Digital platforms connecting producers to global markets are democratizing access in meaningful ways. Historically, small-scale farmers or miners had to sell through middlemen who captured most of the value. Now platforms exist where producers can connect directly with buyers, access market information, and receive fairer prices. I’ve seen cooperatives use these platforms to negotiate better terms and build direct relationships with international buyers. It’s not perfect—digital literacy and internet access remain barriers—but it’s creating opportunities that simply didn’t exist before.

Fintech solutions for commodity financing are addressing another critical bottleneck. Smallholder farmers and small mining operations often lack access to credit, which limits their ability to invest in improved practices or weather commodity price volatility. Mobile money platforms like M-Pesa revolutionized financial access in Kenya and spread across Africa. Now fintech companies are building on that foundation with commodity-specific financing products. I’ve watched farmers use mobile apps to access short-term loans against expected harvests, secured by digital contracts and crop insurance. The interest rates aren’t always great, but it’s access to capital that didn’t exist otherwise.

Satellite monitoring of agricultural production is getting seriously sophisticated and useful. I’ve used satellite data to monitor crop health, predict yields, estimate production volumes, and even identify potential supply chain disruptions before they happen. During droughts or pest outbreaks, satellite data provides early warning that allows supply chain adjustments. Insurance companies use it to verify claims. Buyers use it to plan procurement. The data isn’t perfect—cloud cover in tropical regions creates gaps—but it’s dramatically better than relying on sporadic ground reports or anecdotal information.

AI and data analytics in commodity forecasting have gotten spooky accurate in some applications. Machine learning models can analyze weather patterns, economic indicators, planting data, consumption trends, and dozens of other variables to predict commodity prices and supply availability with increasing accuracy. I’ve watched models predict coffee yield shortfalls months in advance, giving buyers and traders time to adjust strategies. The models still get surprised by unpredictable events—political instability, sudden weather shocks, pandemic disruptions—but for normal market dynamics, they’re becoming genuinely useful tools.

The challenge with all this technology is the implementation gap between pilot projects and scaled adoption. I’ve seen dozens of brilliant technological solutions that work great in controlled environments or limited trials but struggle to achieve broad adoption. Reasons vary: cost, digital literacy, internet connectivity, institutional resistance, lack of standardization. Technology companies often underestimate how challenging real-world implementation is in resource-constrained, infrastructure-limited environments. The solutions that succeed are usually ones that account for these realities rather than assuming conditions similar to developed markets.

Looking forward, I’m optimistic that technology will continue improving African commodity supply chains. Costs keep dropping, connectivity keeps expanding, and a generation that grew up with mobile technology is entering business and agriculture. But technology

alone won’t solve systemic issues like inequality, corruption, or infrastructure gaps. It’s a powerful tool, but only one piece of the larger transformation African commodity supply chains need.

Future Outlook: Africa’s Position in 2030 and Beyond

Trying to predict the future is a fool’s errand, but I’ve been analyzing global supply chains long enough to identify some trends that’ll likely shape where African commodities are heading. By 2030 and beyond, Africa’s position in global supply chains will probably be even more critical than today, though whether that translates into broadly shared prosperity depends on decisions being made right now.

Projected demand for African commodities is honestly staggering. The International Energy Agency, World Bank, and various industry analysts all project massive increases in demand for critical minerals—like we’re talking several hundred percent growth for things like lithium, cobalt, and rare earths. Agricultural commodities will face growing demand from population growth and rising middle classes globally, particularly in Asia. Energy resources will remain crucial during the transition period from fossil fuels to renewables. I’ve seen projections suggesting Africa could account for well over 50% of global supply for several critical resources by 2030. That’s enormous leverage if managed well.

Value addition and industrialization strategies are where African nations could capture dramatically more value from their resources. The traditional model—export raw commodities, import finished goods—has left Africa perpetually poor despite enormous resource wealth. If African countries can build processing capacity, manufacturing capabilities, and move up the value chain, the economic impact would be transformative. I’ve seen national strategies from countries like Ghana, Rwanda, and Morocco that genuinely prioritize industrialization. Others remain stuck in raw commodity export mentality. Which approach prevails will hugely impact outcomes.

Climate resilience and adaptation needs can’t be overstated. Climate change will affect African commodity production more severely than most regions. Agricultural production patterns will shift. Water availability will change. Extreme weather events will increase. I’ve modeled scenarios where major agricultural regions become unsuitable for traditional crops, potentially displacing millions and disrupting supply chains that have existed for generations. Adaptation requires significant investment in research, infrastructure, and support for affected communities. The international community talks about climate financing for adaptation, but actual disbursements haven’t matched rhetoric. This gap needs to close or the supply chain disruptions will be severe.

The potential for economic transformation is real but far from guaranteed. Africa has young, growing populations that could provide demographic dividends—or could create instability if economic opportunities don’t materialize. Technology is enabling new business models and reducing some traditional barriers. Global commodity demand creates opportunities. But transformation requires good governance, strategic investment, infrastructure development, education, and consistent policy frameworks. Some African nations are creating conditions for transformation. Others are missing the opportunity. By 2030, I expect the performance gap between well-governed and poorly-governed commodity-producing nations to be stark and growing.

Risks and opportunities for global supply chains are two sides of the same coin. The opportunity is secure access to resources essential for technology and green energy transition. The risk is over-dependence on supplies from regions with governance challenges, infrastructure limitations, and vulnerability to climate and political shocks. I’ve advised companies to develop diversified sourcing strategies, invest in supplier relationships, and build supply chain resilience even if it costs more in the short term. Those that rely on single sources or don’t invest in resilience will face disruptions—that’s not an if, it’s a when.

Here’s my honest assessment: Africa in 2030 will be more central to global supply chains, more strategically important, and more economically empowered than ever before. But whether that benefits ordinary Africans—the farmers, miners, workers who actually produce these commodities—depends on whether the governance, investment, and development choices made between now and then prioritize broad-based prosperity over narrow elite enrichment. The resources and opportunities exist for genuine transformation. Whether that potential is realized is up to the decisions being made right now. I’m cautiously optimistic but well aware of how many promising opportunities have been squandered in the past.

Conclusion

So here’s where we land after this deep dive into African commodities and global supply chains: Africa isn’t just participating in the global economy anymore—it’s literally holding some of the most critical keys to our technological and environmental future. From the cobalt powering your devices to the coffee kickstarting your morning, from the platinum in catalytic converters to the cocoa in your chocolate, African commodities are woven into the fabric of modern life in ways most people never realize.

The transformation I’ve witnessed over my career has been remarkable. Africa has moved from being seen as a peripheral economic player to being absolutely central to supply chain strategies of major corporations and nations. The demand for critical minerals for green energy transition, the strategic importance of agricultural exports, the energy resources reshaping power dynamics—all of this positions Africa as increasingly indispensable to global prosperity. That’s power, if wielded strategically.

But here’s the thing that keeps me up at night: resource wealth alone doesn’t guarantee prosperity for ordinary people. History is littered with resource-rich nations that remained poor while elites and foreign corporations extracted wealth. For African commodity dominance to translate into broadly shared development, we need ethical sourcing practices, fair value distribution, good governance, infrastructure investment, and value addition that keeps economic activity on the continent. That requires commitment from African leaders, responsible behavior from international corporations, and pressure from conscious consumers.

I’ve tried throughout this article to be honest about both the opportunities and the challenges. The potential is enormous, but so are the obstacles—infrastructure gaps, governance issues, ethical concerns, climate vulnerability, geopolitical competition. Transformation isn’t inevitable; it requires deliberate choices and sustained effort from all stakeholders.

For businesses and investors reading this: Africa’s commodity supply chains will be central to your operations and strategies for decades to come. Invest in relationships, build resilience, prioritize ethical practices, and think long-term. For consumers: the products you use every day depend on African resources extracted in conditions you should understand and care about. For policymakers: supply chain security requires engagement with African nations as partners, not just as sources of raw materials.

The story of how African commodities shape global supply chains is still being written, and we’re all participants whether we realize it or not. I’m curious to hear your perspectives—have you seen these dynamics play out in your industry? Are you making purchasing decisions based on sourcing ethics? What do you think needs to happen for African commodity wealth to translate into broadly shared prosperity? Drop your thoughts in the comments; I genuinely want to hear different perspectives on this complex, critical topic. The future of global supply chains is being built right now, and understanding Africa’s central role in that future isn’t optional anymore—it’s essential.